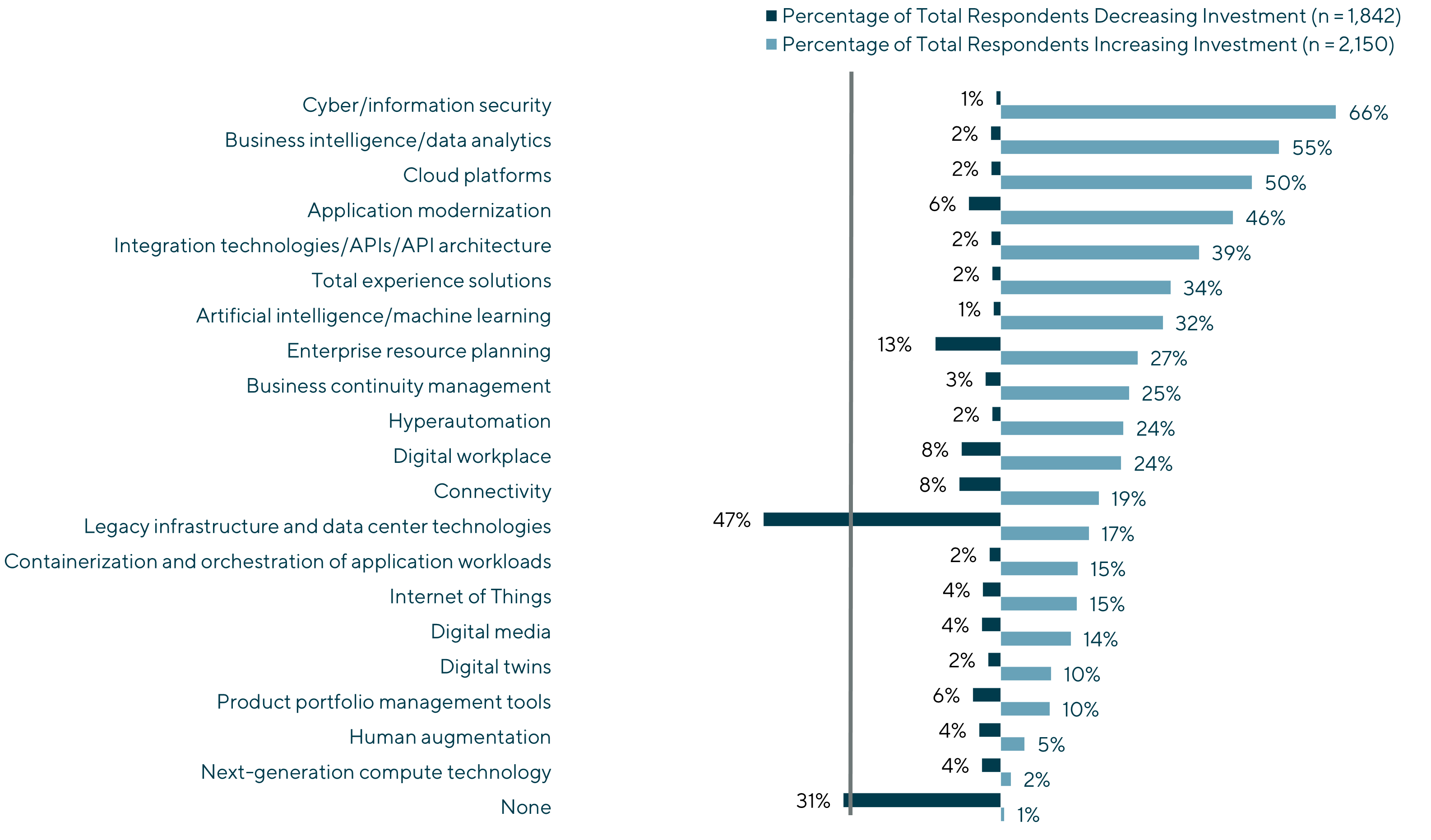

Figure 1

Source: 2023 Gartner CIO and Technology Executive Survey

Deal Thaw will Accelerate in 2024

We see the pipeline of M&A and investment processes preparing to go to market lengthening, and our market checks show definitive itchiness by investors and strategics to deploy capital. Further, as we reported in Q1, the pool of cyber buyers (as defined by the number of relevant strategics with > $100 million revenues) has expanded by 75% over the past three years, reflecting the impact of $165 billion of expansion capital deployed by investors and acquirers in cyber just since 2021. There is also a record number of initial public offering-worthy cyber unicorns (>50) waiting in the wings for the public capital markets to reopen, creating a new pool of growth capital and liquid stock for further acquisitions.

Intensifying Vendor Collaboration to Benefit those with Partnering Virtuosity

RSAC’s ‘Stronger Together’ theme alludes to the value of alliances, more of which were announced than at any prior RSA conference. Presenters spoke of a pressing need for integration across three capability spectrums: visibility (endpoint, network and cloud), time (before, during and after attack) and function (human / manual – AI / automation). CrowdStrike emphasized increasing attack sophistication as necessitating the embrace of a holistic, shared approach to security. Cisco discussed the value of information-sharing among vendors, government and cyber professionals to address the evolving threat landscape. Accenture announced an alliance with Palo Alto Networks to combine extended detection and response, AI and know-how. In addition to placing a premium on vendors that play well with others, it also benefits those with unified platform offerings.

M&A Consolidation to Accelerate Within, Rather than Across, Segment Stacks

While surveys suggest that organizations seek to reduce the number of cyber vendors they utilize, the goal is not cost-cutting, but greater efficacy. Consequently, we see acquisitions focused on creating function-defined platforms – resulting in category powerhouses, rather than supermarket-style consolidators like the Symantecs and McAfees of the olden days. Platform stack leaders are forming in areas that notably include cloud workload security, data security, attack surface management, identity and access management, security service edge, extended detection and response and integrated risk management.

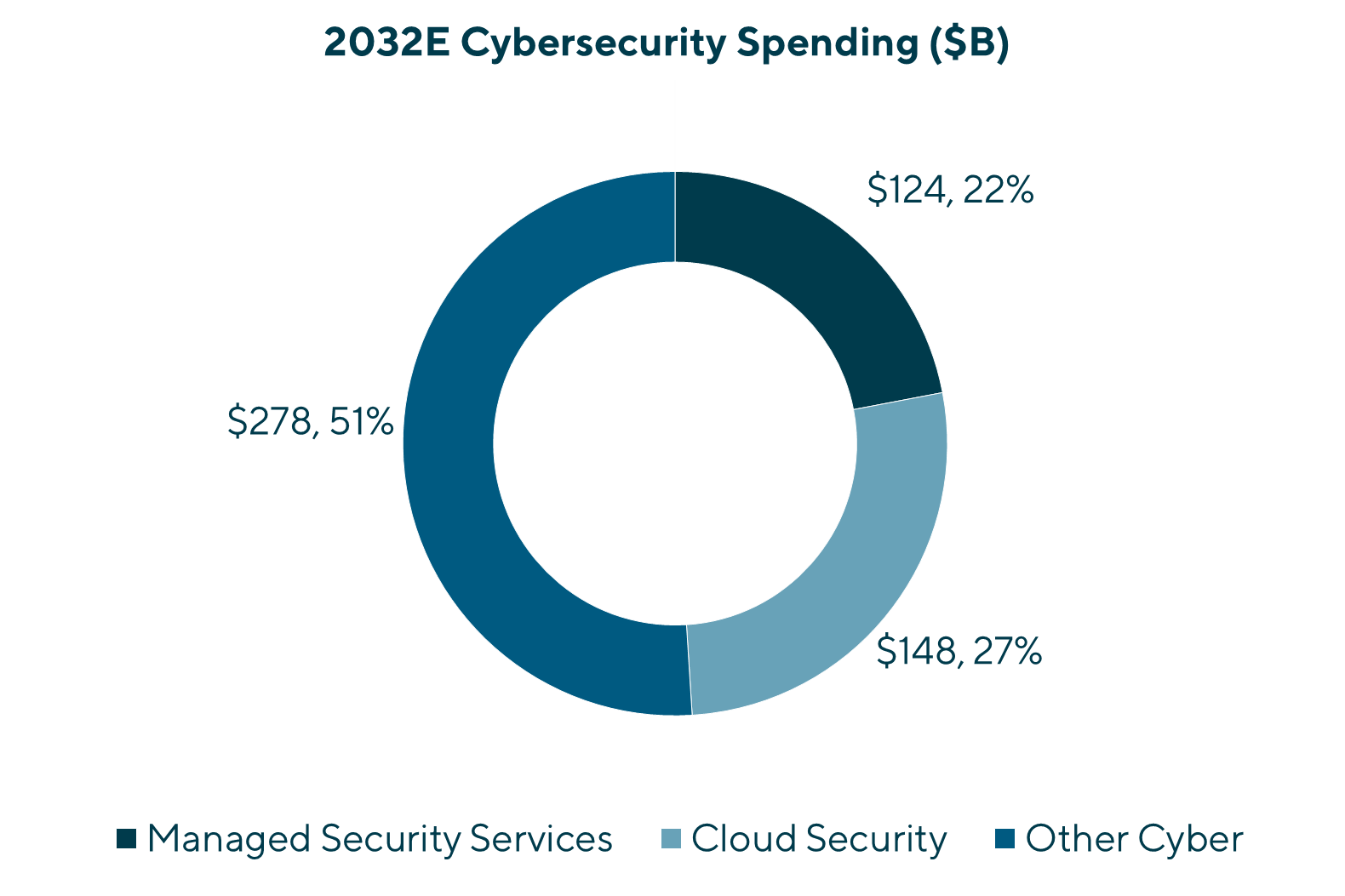

Managed Security Services and Cloud Security to Dominate M&A and Investment Activity

Within a decade, we estimate that half of total annual cyber spending will run through managed security services and cloud platforms (see figure 2). Hence, acquirer and investor activity will be over-indexed toward these areas. In managed security (managed detection and response / managed security service providers) for example, billions of dollars in anchor private equity investments have been made recently to create and grow platforms (e.g., ArcticWolf, Avertium, BinaryDefense, Blackpoint, BlueVoyant, CriticalStart, DeepWatch, eSentire, Expel, Red Canary and ReliaQuest). This is similarly seen in big investments in cloud-based security platforms (e.g., Apiiro, CipherCloud, Coro, Lacework, Netscope, Panther Labs, Orca, Snyk and Wiz).

Figure 2

Sources: Allied Market Research, Market.us, Transparency Market Research and Fortune Business Insights

AI Emergence in Cyber is Real and Rapid

AI was the most ubiquitous discussion topic, both at RSA 2023 and June’s Gartner Security & Risk Summit, revolving around how vendors and customers plan to integrate it into their cyber planning. While concerns surrounding AI’s benefits to cybercrime are great, the consensus is that the new capabilities will be a net positive for enhancing threat detection and incident response. Annual global spend on AI-based cybersecurity products is predicted to reach $97 billion by 2032, and will be seen largely in the form of solution upgrades rather as new security categories or AI-pure plays. This will energize replacement and upsell cycles. We see vendors already including AI plans in development roadmaps as more than 70% of organizations will have generative AI embedded into security operations within the next five years.

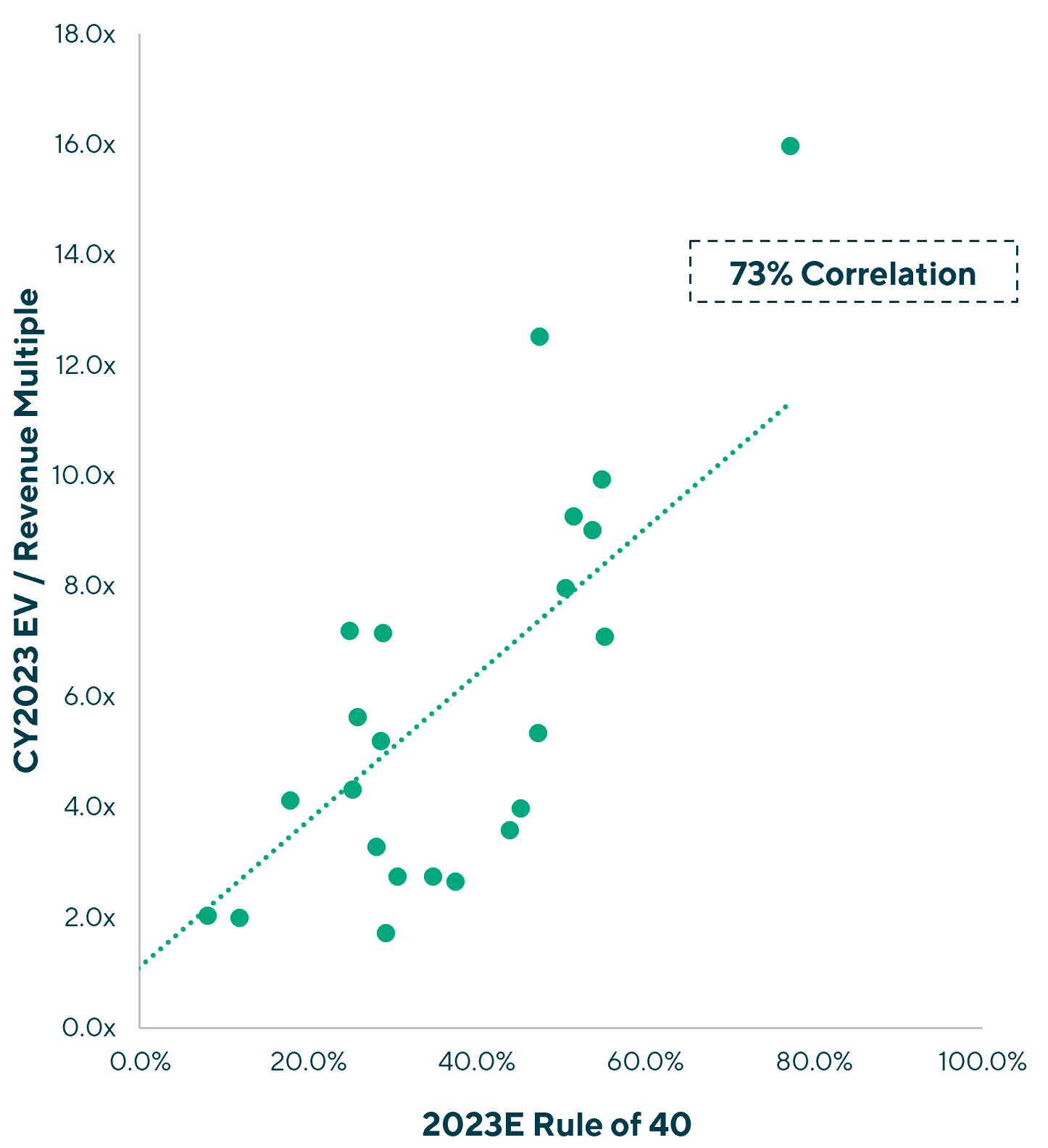

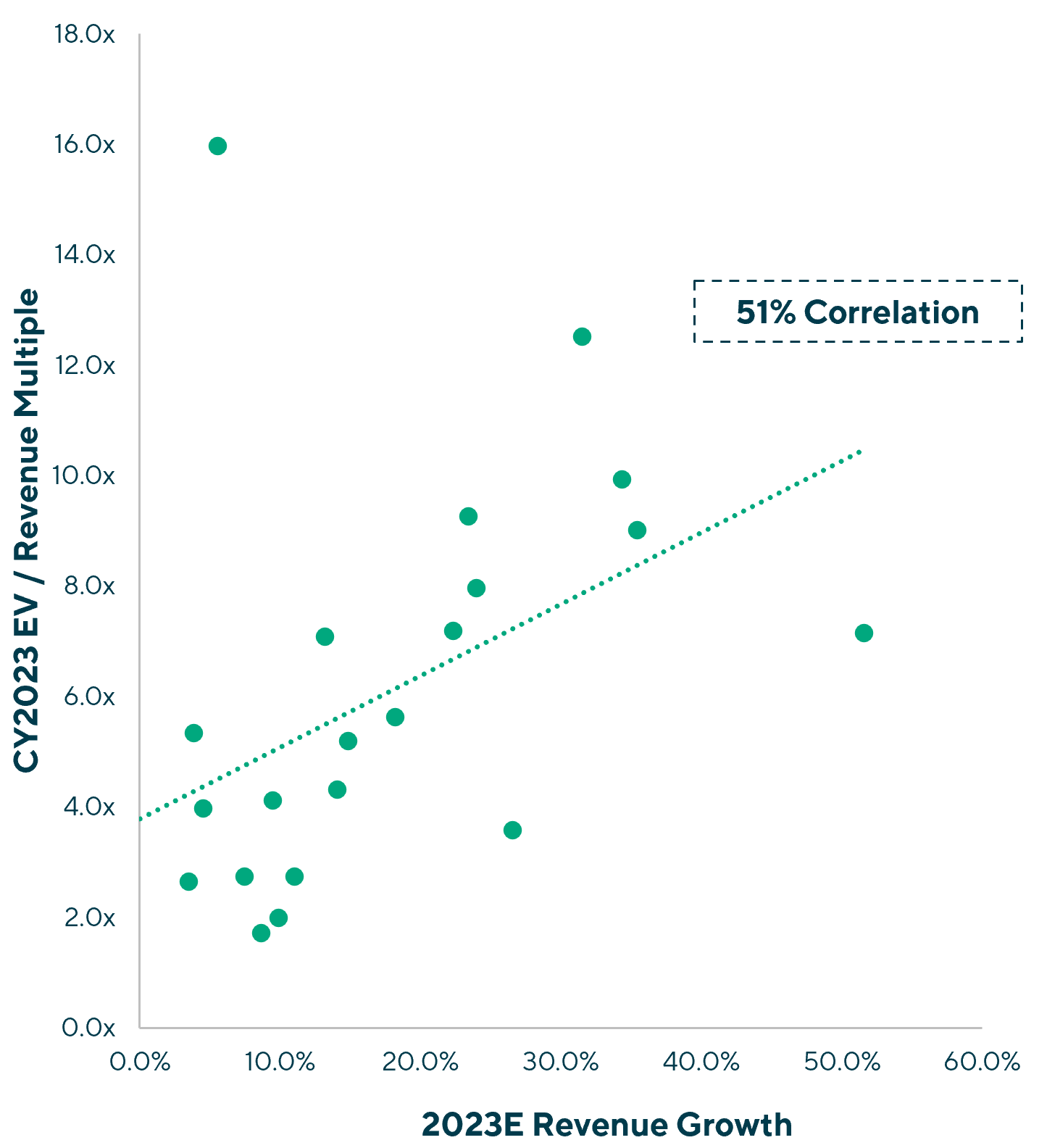

Rule-of-40 has Permanently Displaced Revenue Growth as the Industry’s Primary Value Driver and Correlator

For more than a decade until late 2021, the cyber industry’s strongest predictor, by far, of vendor valuation (utilizing R-squared coefficient of determination), was short-term projected revenue growth. For example, a scatterplot of publicly traded cyber vendors’ enterprise value / next-year estimated revenues versus next-year estimated revenue growth rates routinely generated R-squared values exceeding 0.7. This means that greater than 70% of a cyber vendor’s value was determinable by its near-term revenue growth rate. Performing the same analysis using Rule 40% rather than revenue growth (enterprise value / next-year estimated revenues versus [next-year estimated revenue growth rate + EBITDA margin]) resulted in a much lower correlation, typically in the 40% range, meaning that EBITDA profitability actually reduced valuation multiples. Today–and this has been the case for over a year–the correlations are reversed, so that Rule of 40%, which considers profitability, is a much better predictor of valuation than revenue growth alone (see figure 3). The significance of this shift is that future investments will be geared toward driving profitability, even at the expense of growth. This is seen in the sharp change in public vendor performance just since last year. In 2022, three of 25 U.S. publicly traded cyber vendors were EBITDA-positive, and in 2023 the Street projects that 23 of 25 of these vendors will be profitable, while median annual revenue growth is expected to halve. The implications are already being seen in the private markets, with investment capital shifting to support near-profitable and cash-flow-positive cyber businesses. This has resulted in lower revenue valuation multiples as well as lower revenue growth rates as companies retool operations; these multiples however will stabilize and start rising as more companies turn profitable and funnel cash flow to more durable growth models.

Figure 3

| Rule of 40(1) versus Enterprise Value / Revenue Multiples

|

Revenue Growth versus Enterprise Value / Revenue Multiples

|

Source: Market data sourced from S&P Capital IQ as of 05/10/2023

(1) The Rule of 40 is calculated as 2023 projected revenue growth plus 2023 projected EBITDA margin

Contributors

Meet Professionals with Complementary Expertise

I am inspired by working with entrepreneurs and innovators who feel passionately about what they are creating.

William Bowmer

Managing Director & Co-head of Technology, U.S.

San Francisco

I deliver a hands-on approach to provide strategic advice to my clients throughout the transaction and beyond.

Chris Brooks

Managing Director & Co-head of Technology, Europe

London

Related Perspectives

Recent Transactions

Cybersecurity: Zeroing in on Current and Future Trends

As we enter the second half of the year, the state of cybersecurity is coming into sharper focus following a tumultuous 2022. Here are Lincoln International’s key observations and predictions.… Read More

IPEM | Event: Cannes 2023

Lincoln International was pleased to attend IPEM Cannes 2023 from January 23 to 25. The event provided attendees the opportunity to connect with other professionals in the private capital markets,… Read More

Whither Cybersecurity Deal Activity in 2023?

Don More, Managing Director in Lincoln International’s Technology, Media & Telecom Group, recently attended Evolution Equity Partners’ Annual Investor Day in New York to discuss the capital markets and cybersecurity… Read More

Software Sector Shows Resilience in Recurring Revenue Financing

Amid recessionary pressures, the software sector has proven resilient with low default rates and healthy cash flows for most companies. Lenders continue to see opportunities with software companies—even those with… Read More

All Systems Protected? Cybersecurity Trends in 2022

Accelerated digitalization post-COVID-19, convergence of cyber and military power projection and the increasingly complex threat environment are forcing rapid transformation of the cybersecurity industry. Organizations are hungry to protect systems… Read More

Adopting Alternative Strategies – How Partnering Expertise Can Help

Company leaders around the globe are facing uncertain business conditions, including geopolitical tensions, inflation, continuing supply chain problems and raw materials shortages. Economies are only just beginning to recover from… Read More

Business Leaders Adjust Investment Strategy in Light of CO2 Emissions Standards

As governments and company stakeholders continue to increase their focus on reducing emissions, the shift from fossil fuels to green energy is shaking up almost every sector—resulting in energy efficiency… Read More

Private Equity Pursues Investments in Engineering and Manufacturing Software Sector

Engineering, simulation and manufacturing software is in high demand as companies across industries shift toward digitizing processes. From the early stages of product design and simulation to manufacturing and usage… Read More

Growing Local & Global Private Equity Interest in French Technology

The technology ecosystem in France is booming. In 2021 alone, French startups raised more than €10 billion in venture capital financing, a 2x increase over 2020. To date, the number… Read More

M&A Activity Remains Strong for Companies Supporting Employer-Sponsored Health Benefits

Employer-sponsored, self-funded medical plans have grown in popularity since the implementation of ERISA in the 1970s and now cover nearly two-thirds of all employees and one-third of all Americans. Medical… Read More

Data Center Download: Accelerating Growth, Record Interest in the Space and Transformational Opportunities

Our world has become more reliant than ever on data. As technological innovation stretches from the smartphones in our pockets to wearables, self-driving cars, cloud computing, artificial intelligence, Industry 4.0… Read More

Cybersecurity M&A Momentum: Digitalization to Drive Accelerated Demand and Total Available Market Expansion

As C-suite executives focus intensely on corporate digital transformation efforts, cybercriminals are following suit and adjusting tactics to exploit the resulting massively broader cloud attack surface. This big new challenge… Read More

“Play On” – Investing in the Post-COVID-19 Pandemic Experience Economy

As we come to terms with the lasting impacts of the COVID-19 pandemic, it’s fair to say we have entered a new age in the consumer economy. While nearly all… Read More

Animal Health Players Pursue Vertical Integration as a Path to Growth

Animal health businesses that have established a strong presence within their area of expertise, may be considering where the next best path to growth lies. While cross-border expansion and consolidation… Read More

PE News | Debt Funds Seek Ways to Fund the Adoption of Technology

Originally published by Private Equity News on September 20, 2021. Xenia Sarri, Managing Director in Lincoln’s Debt Advisory Group, discuss with PE News on how Covid has created a spike… Read More

E-commerce, Sustainability and Digital Capabilities Drive Consolidation

Following a rebound in the first half of 2021, the outlook for the economy remains positive for the second half of the year as vaccination rates continue to climb and… Read More

Our Economy Runs on Digital: Fueling Infrastructure Software Investment

As companies continue to move to the cloud and provide high-quality, global-scale cloud solutions, infrastructure software has seen a material increase in investment and consolidation, as evidenced by recent sponsor-led… Read More

Order Up: Dramatic Change in Consumer Behavior Drives Accelerating Need for Restaurant Technologies

Fleet, Field and Asset Management Software: Convergence Creates Investment Opportunities

Maintaining equipment, vehicles and other assets while also optimizing performance of employees and the work they do is a daunting task for any organization. To address this challenge, both large… Read More

Q&A with Lincoln TMT Managing Director Don More: Hacking Cybersecurity Investment

Lincoln International recently welcomed Don More as Managing Director focused on Cybersecurity on the Technology, Media & Telecom team. Don brings to Lincoln 20+ years of deal experience in cybersecurity,… Read More

Doing Well While Doing Good: Profiting from Non-Profit Tech

Non-profit organizations (NPOs) are increasingly adopting new technology solutions as they aim to provide efficient services, spawn innovation and attract the donations that are critical to their existence. The NPO… Read More

Bright Spot: The Sun Shines on Solar Energy Investment

Renewable energy generation is a growing priority for countries across the globe. In 2015, 196 parties adopted the Paris Climate Agreement and in 2021 the United Nations Framework Convention on… Read More

No EBITDA, No Problem: Software Financing and the Rise of the Non-Bank Lender Market

The technology sector has been a bright spot for years. Even during the challenges created by the pandemic, our Lincoln International M&A bankers are seeing record levels of software investments… Read More