Powering Utility & Infrastructure Services M&A Activity in a COVID-19 Landscape

Apr 2020

Last month, the Cybersecurity and Infrastructure Security Agency (CISA), along with other federal agencies, state and local governments and the private sector, created an advisory list of “Essential Critical Infrastructure Workforce.” This list helps ensure the continuity of functions critical to public health and safety, as well as economic and national security, while encouraging non-essential workers to practice social distancing to slow the spread of the novel coronavirus (COVID-19).

The Essential Critical Infrastructure Workforce includes workers who provide services that are deemed essential to the ongoing viability of vital utilities, including natural gas, power and telecommunications. These services include, but are not limited to, maintaining, repairing and installing infrastructure, executing construction and performing operational functions.

For companies deemed essential, the priority is employee safety and compliance with guidelines from the Centers for Disease Control and Prevention (CDC), the World Health Organization (WHO) and the Occupational Safety and Health Administration (OSHA). Accordingly, service providers that successfully balance employee welfare and service delivery, while simultaneously supporting customers’ most critical needs, should perform exceptionally well in the challenging COVID-19 landscape.

| Lincoln Perspective

There may be a modest dip in demand for utilities during COVID-19 as non-essential businesses close; but individuals working from home and other critical businesses – from hospitals to factories– still need access to these services. The resultant non-discretionary demand will enable businesses supporting these critical utilities and related infrastructure to outperform other sectors, both in the near-term and over the longer-term. The capital budgets of most businesses are expected to be severely impacted as companies seek to protect liquidity and cash flow during the COVID-19 crisis. However, “rate cases” provide power and natural gas utilities a built-in funding mechanism for infrastructure maintenance and replacement. Regulated utilities seek rate cases from public utility commissions on a periodic basis to cover the costs of planned, and often necessary, infrastructure upgrades, maintenance, repairs and replacements. Rate increases are justified if the infrastructure replacement improves public safety, system reliability, lessens environmental impact or reduces the cost to ratepayers over time as system performance is enhanced. Since they earn a return on such investments, utilities are incentivized to invest in infrastructure upgrades. The resulting spend is relatively non-discretionary and less susceptible to economic downturns – attracting the attention of private equity investors. Other important factors driving private equity to consider M&A in this sector include the opportunity to consolidate a fragmented market typically comprised of regional or local businesses, expand geographically and build a platform of broader utility service lines. We expect the industry’s resiliency and strong long-term fundamentals will continue driving investor interest, especially when the debt financing markets fully stabilize following COVID-19. More specifically, the following three sectors have our attention: |

|

|

1 |

Natural Gas

Natural gas consumption is projected to grow across residential, commercial and industrial applications at a faster rate than the rest of the energy sector over the next few decades as it is a lower cost, safer and more environmentally sensitive alternative to propane, fuel oil and electric heat. Despite natural gas’ appealing characteristics, over the last decade, antiquated infrastructure has been the cause of multiple high-profile leaks, including explosions in California in 2010, several in New York City between 1996 and 2015, and Northeastern Massachusetts in 2018. All of these events involved fatalities, injuries, service disruptions and significant property damage. As such, multiple federal- and state-level initiatives have prioritized the replacement of natural gas distribution pipelines, requiring utilities to expedite the replacement of high-risk mains and service lines. With public safety, and to a lesser extent environmental concerns, driving regulatory actions on required infrastructure investment, it is unlikely that the economic cycle will pause such initiatives. Pipeline safety is particularly relevant in the Northeast and Mid-Atlantic as these geographies operate some of the oldest gas distribution grids in the country. The country has 2.6 million miles of pipeline, many of which need to be replaced. The sheer size and scale of the necessary updates substantiates decades-long work for utility and infrastructure service providers. |

|

2 |

Power

Most of the power transmission and distribution infrastructure in the United States was built decades ago and incorporates technology developed in the mid-20th century. Since the national electrical grid was built, growth in electricity demand has far outpaced the expansion of the network’s usage. From 1988 to 1998 alone, demand rose 30% while capacity increased by only 15%. Historical underinvestment in the electrical grid has resulted in congestion, outages and unreliable power delivery. It is projected that power outages annually cost the U.S. economy as much as $150 billion. Notably, unlike the natural gas market, opportunities in the power sector extend beyond the utility grid and into a facility or building’s “four walls.” To mitigate the risk of injury from faulty equipment, including potentially fatal arc flashes, safety regulations from OSHA and insurance companies require routine diagnostics, testing and preventative maintenance of power distribution and control equipment (e.g., transformers, switches, circuit breakers). The country’s aging infrastructure and heightened safety standards are supported by other industry tailwinds, including numerous regulatory actions that are motivating utility companies to make necessary infrastructure investments. Additionally, utilities continue shifting towards an outsourcing strategy for maintaining transmission and distribution infrastructure. Benefits of using third-party service providers include lower cost, higher productivity, greater flexibility, faster response times, improved safety and a reduced fixed cost burden. |

|

3 |

Telecommunications

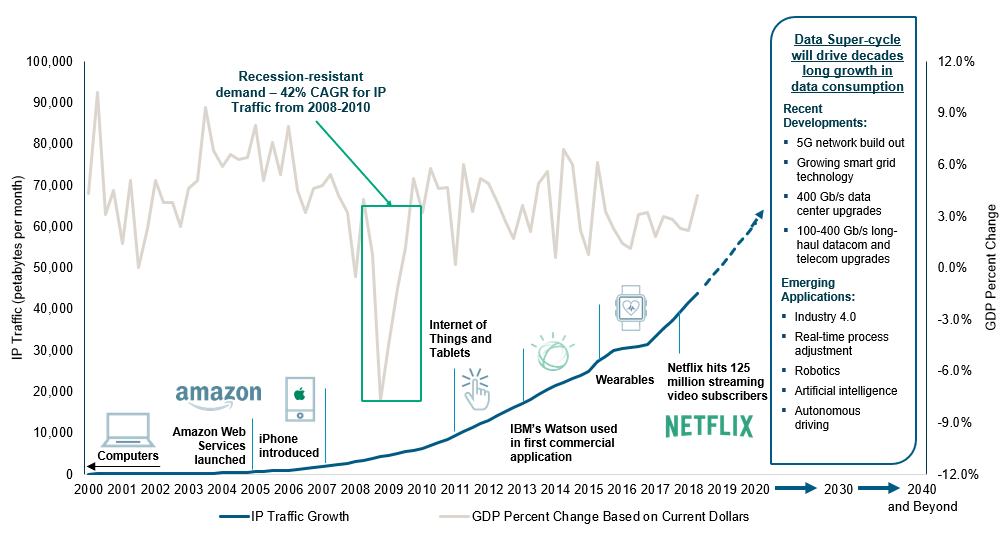

Today, perhaps no utility is under a greater microscope in the United States than telecommunications. With a tremendous surge in people working from home, schools shifting to virtual classrooms and the rapidly growing use of streaming services, there is an immediate need for service providers to maintain and support the integrity of their respective networks. In addition, multiple industry tailwinds, illustrated below, will drive unprecedented demand for data moving forward – making data consumption recession-resilient. Data Consumption Will Continue to See Exponential Growth and is Recession Resistant

Source: U.S. Telecom, The Broadband Association; Cisco Visual Networking Index; U.S. BEA Even before COVID-19, U.S. mobile carriers were planning substantial investments in the deployment of hyper-fast wireless internet in the next several years. Then, social distancing caused by COVID-19 placed a significant premium on remaining professionally and socially connected. As a result, there will be even more significant investment in the country’s broadband infrastructure. On March 12, Verizon said it will boost investment in network infrastructure, increasing its capital guidance for 2020 by $500 million, to as much as $18.5 billion, in part, to accelerate the company’s transition to 5G. Then on March 20, AT&T withdrew its $4 billion stock buyback program. In its regulatory filing, AT&T cited the need to enhance its network, including 5G investment, among other reasons. Though there may be some short-term hurdles in the rollout of 5G technology, the arms race between Verizon and AT&T will create substantial opportunities for the installation, maintenance and repair of networks by third-party service providers for years to come. |

Summary

-

Lincoln International's Energy, Power & Infrastructure Group discusses factors driving M&A activity in the industry and the long-term fundamentals that will continue driving investor interest in a COVID-19 landscape.

- Click here to download a printable version of this perspective.

-

Lincoln International has created a Playbook to support business leaders in documenting and articulating their COVID-19 response. To request a copy, click here. - Sign up to receive Lincoln's perspectives