Pitchbook | Q&A: The Evolution of Medtech in a Globalizing Industry

May 2019

View original post from Pitchbook on May 29, 2019 here. ![]()

Multiple industries are still globalizing inexorably, even given the intensification of the US/China trade dispute. Medical technology is no exception, driven by advancement of healthcare in emerging markets, global aging demographics, pricing pressures and a focus on cost effective products and solutions. In a wide-ranging Q&A with four global Lincoln advisors, we assess medtech’s evolution and the potential horizon for cross-border deals in the hot sector.

What is driving the interest in medtech M&A and what are investors experiencing vis-à-vis challenges as they capitalize on the momentum?

Ross: One of the key factors driving interest from newer entrants and private equity buyers is that they are seeking the growth and margin profile that the medical technology sector offers. They are attracted to medical technology platforms that offer strong growth and attractive margins that are recession resistant. A primary hurdle is ensuring that the potential target has a strategic or differentiated position in its market niche and/or has the necessary sales, marketing and distribution capabilities. For context, many medtech segments have seen consolidation around complete care episodes and product bundling, so it is critical that a non-traditional buyer or a financially-oriented buyer has the required channel access to succeed.

Ikuo: The evolution of specialist medtech companies with more focus on surgical/treatment instruments, especially those that are minimally invasive, has encouraged acquirers’ interest. Precision equipment/device manufacturers (such as Topcon and Nikon) are also expanding medical equipment/device business through acquisitions, in order to capture higher-margin, higher-growth opportunities. In addition, recently pharma companies are looking for medtech targets with a view to combining the traditional Rx business with medtech (hardware and software) so as to bring a comprehensive healthcare “solution”.

Matt: The large corporate players continue to focus on growth, focusing their M&A on new products, intellectual property acquisitions or deals that give new geographic and market access. After a number of deals we will often see that corporates have built up considerable portfolios of assets, some with overlapping technologies or divisions. As with any large corporate, the tail can begin to underperform given lack of focus, driving the potential for the owners to consider carve-outs or disposals to refocus the portfolio. These opportunities can often be of interest to private equity funds. We are seeing medical device businesses as increasingly of interest versus the broader healthcare services space, which is often seen as very dependent on single markets or central organizations and/or funders like the NHS in the UK or Medicare / Medicaid in the USA. In contrast medical device companies benefit from a globalized customer base, attractive both for growth and reducing customer risk, all while supported by common macro drivers such as aging populations. A good recent example of PE interest in medical devices we’ve just worked on, albeit not a carve-out, is a UK wound-care business called Medtrade Products which took on investment by Tikehau Capital. We acted as advisors for Tikehau Capital who are providing some liquidity to the shareholders while investing additional capital to grow the business in new markets and help bring new products to market.

Has interest increased in acquisitions over the past several years by large multinational corporations in Asia, and vice versa?

Ikuo: As Japan is still in the process of developing a medtech venture ecosystem (with spinouts from large corporates as well as entrepreneurs out of academia), Japanese strategics tend to look for the US (the most dynamic medtech market in the world) and Europe for acquisition opportunities. Typically, what is sought after is technology/products being developed by medtech companies in these countries. If Japanese strategics already have an existing distribution platform in the US or Europe, addition of products may suffice. If, on the other hand, they cannot utilize such platform, they seek medtech companies with technology/products combined with marketing capabilities. In addition to developing a business in the US or Europe, they want to import the technology/products of the acquired company back to the Japanese market, where the ageing population requires provision of high-quality yet efficient medical services.

Gaurav: India’s space is still currently dominated by the largest class of US and European multinationals, from Danaher to Becton Dickinson, which retain substantial presence across multiple channels from marketing to production. That looks set to stay in place for mature M&A targets within the foreseeable future. The Indian mid-market is rather small still, so their primary focus tends to be the startup and emerging growth scene. There can be some exceptions, where larger players from outside the Indian market look to acquire local manufacturing and/or distribution centers, but generally the primary strategic incentive is to absorb younger companies with worthwhile technical innovations.

Among the Indian healthcare-related startup scene, which segments are specifically drawing the most interest from prospective acquirers?

Gaurav: Most of the viable startup interest is concentrated in the diagnostics space, where companies can utilize the basic sensors even within smartphones to collect and analyze information. Many of the companies are very young, so there is still a significant amount of development to occur. Areas with larger startup costs—such as orthopedics, implantables, etc.—are still more dominated by established players.

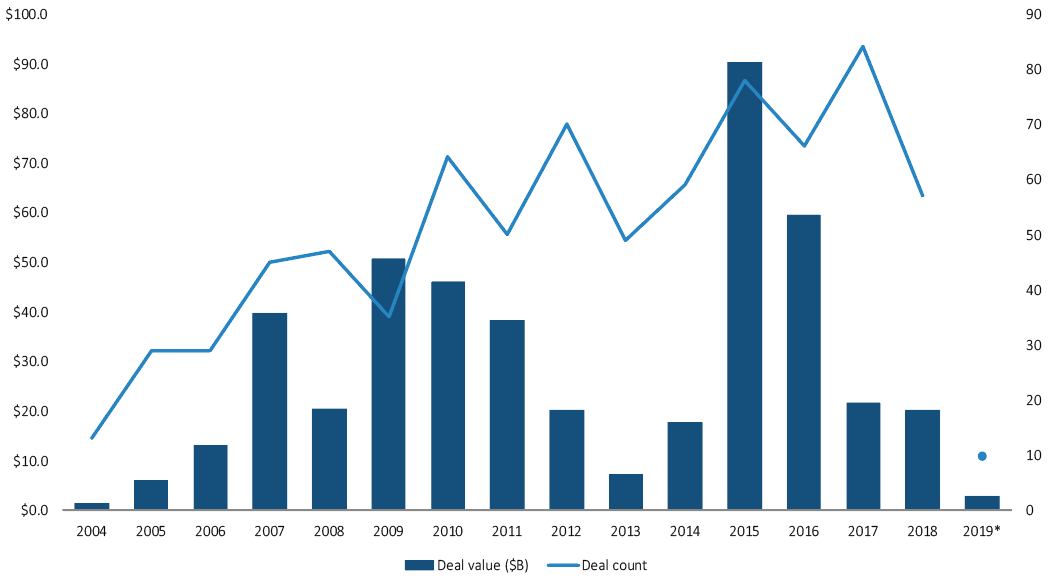

What is helping drive increasing cross-border activity within medtech, as PitchBook data reveals?

Ross: There has been significant consolidation in recent years among the leaders in the medtech sector—with Medtronic-Covidien, Abbott-St Jude Medical and Becton Dickinson-CR Bard as a few examples. Consolidation among the top players results in fewer “typical” buyers by definition. While the market leaders, many of which are US-based, will certainly continue to be acquisitive, there is strong and growing interest from buyers outside the US looking to both access US markets as well as build leadership positions in other key medtech geographies including Japan and China. In addition, there is strong cross-border activity in the medical device outsourcing sector, where non-traditional buyers seek acquisition opportunities that provide more exposure to the medtech sector.

How are prospective buyers handling regulatory challenges, especially when it comes to cross-border M&A activity?

Gaurav: One key factor that I should mention that pertains to potential future is the regulatory incentive for medtech players to potentially consolidate or set up local manufacturing and/or distribution centers. Recently, price caps on imported medtech products have impacted profit margins for global medtech manufacturers, e.g. the gap between the price prior and after can range up to 20%. That could spur some future M&A as global entities look to establish domestic manufacturing operations.

Ross: Different geographies have disparate regulatory pathways, so there can be differing timelines and elements of risk to take into account; for example, approval in one market does not entail a long lead time compared to approval of that same product in a different market. That said, some products can obtain faster routes to approval given the credential of US approval; it is a complex dynamic that buyers must be attuned to.

Matt: The natural route for many medical device businesses outside in the UK or Europe is to focus on the CE mark approval process initially, which is helpfully standardized across the EU under the Medical Device Directive (MDD), albeit changing, and gives access to a the large market which is the EU. The CE mark is quicker than FDA 510(k) to gain and often based on clinical evaluation of published data for existing equivalent devices. Getting reimbursement approval is the next and different challenge, especially given centralized procurement bodies. Businesses like Deltex Medical and Lidco Group, even though small companies, have pursued approval in the US market and Japan given their potential for growth and the challenges in the UK given funding pressures. Given changing and lengthy product approval processes, and clinical trials for FDA approval, along with reimbursement approval processes, M&A can be a way to shortcut this and acquire a product already in market or gain know how to fast track a similar product. M&A also helps diversify regulatory and reimbursement risk as you build a broader market/geographic presence.

In closing, what are the key underrated trends characterizing cross-border dealmaking, against the context of the globalizing medtech space?

Gaurav: Managing people and relationships in Indian dealmaking is especially critical. Differences in business cultures, practices and strategies exist and must be anticipated and handled during a transaction. For example, potential acquirers often diverge into two schools of thought, where the former seeks to replace a founding team entirely, and the latter wishes to keep them in place. Given the characteristics of the Indian market, the latter is usually a better practice. As always, regulatory risks also must be noted.

Ross: Gaurav’s points are excellent. The nuances of how negotiations are conducted in cross-border dealmaking are often not given the care required to deliver a successful transaction. Different cultures have varying style dynamics that can play into how not only deals are done but also how companies are managed post-close.

Matt: It’s difficult to say given there are so many sub-sections of the market which have unique drivers to each. The aging population will continue to drive most markets and technological advancement will increase the scope of what is possible. Against this, funding bodies are becoming more stringent on proof of ‘value add’ so you see some OEMs like Medtronic starting to move into services as a way to support client system efficiency / ‘cost out’, while also promoting their products into the same customer base. Medtronic did this in the UK with the University Hospital of Manchester NHS for cardiology. I would expect more of this in the future and more service-related moves by medical device corporates alongside a rationalization of large portfolios built up through M&A.

Ross: There is some discussion in the industry right now about how to handle any potential disruption to medtech supply chains given trade disputes between the US and China. China will continue to be a critical market both for supply chains as well as in the context of China being a key market with large and growing local demand. However, other low-cost manufacturing geographies, including Mexico, Costa Rica and Puerto Rico, are playing a critical and growing role in the medical device supply chain and they will continue to do so. Furthermore, another trend which has been interesting to observe is the increasing cross-border activity among nations not involving the US, as US nationalism and greater restrictive oversight to M&A and cross-border activity is driving countries like China to pursue business relationships and investments in other geographies for advanced technologies, including countries and geographies like Israel, Japan, Korea and the EU.

Matt: Similar to Ross’ point, Brexit here in the UK/Europe is a big discussion point naturally. We are seeing many players having to prepare for the unknown, with some UK clients now investing in warehouses in the EU and stockpiling to ensure they have supplies available should transport logistics be impacted. Companies’ capital structures and balance sheets are therefore being impacted which we see in M&A deals through diligence work. Volatility in foreign exchanges also is something that has been front of mind for UK medical device corporates who are often selling in US dollars or Euro and have British Stirling cost bases.

Summary

-

Lincoln International professionals explore what is driving the interest in medtech M&A and what investors are experiencing vis-à-vis challenges as they capitalize on the momentum.

- Has interest increased in acquisitions over the past several years by large multinational corporations in Asia, and vice versa?

- Among the Indian healthcare-related startup scene, which segments are specifically drawing the most interest from prospective acquirers?

- What is helping drive increasing cross-border activity within medtech, as PitchBook data reveals?

- How are prospective buyers handling regulatory challenges, especially when it comes to cross-border M&A activity?

- What are the key underrated trends characterizing cross-border dealmaking, against the context of the globalizing medtech space?

- Sign up to receive Lincoln's perspectives

Healthcare MedTech Experts & Contributors

Professionals with Complementary Expertise

I enjoy working closely with clients to overcome challenging situations and to develop strategies to meet their business goals.

Dirk-Oliver Löffler

Managing Director | European Co-head Healthcare

Frankfurt

Related Perspectives

PETS International | Consolidation Meets Regulation in the Veterinary Clinics Market

Originally posted by PETS International on April 5, 2024. Animal health is becoming a big business in Europe and the U.S. Thus, regulators are turning a closer eye to mergers… Read More

“Leader to Leader” Series

The Leader to Leader video series turns up the dial on rich conversations with prominent leaders – from business owners and entrepreneurs to investors and CEOs – highlighting their stories… Read More

What Price is Right? Trends and Opportunities for Private Equity in Pharma Market Access

The cost of developing new drugs is staggering. Among the top 20 global biopharmas, the average cost of developing a candidate from discovery through clinical trials to market was approximately… Read More

Investment Opportunities in Pharma: A Data-Driven Exploration of CDMO Appeal

The report discusses the current state of the contract development and manufacturing organization (CDMO) market within the pharmaceutical industry, emphasizing the increased interest from private equity (PE) investors. The pharmaceutical… Read More